Can a single buyer still buy an apartment in Brussels without overstretching?

Single buyers now account for a large share of logements vendus in Bruxelles, with La DH reporting that 52% of homes sold in the capital were bought by people classified as “célibataires”. The practical takeaway is simple: for a solo buyer, an apartment is often the more realistic first purchase than a house, but the decision should be built around total monthly cost, registration duties, commune choice and long-term mobility rather than headline price alone. Brussels remains Belgium’s most expensive region for houses, while apartments offer a lower entry point and more choice in communes such as Anderlecht, Molenbeek-Saint-Jean, Jette, Ganshoren and Saint-Josse-ten-Noode.

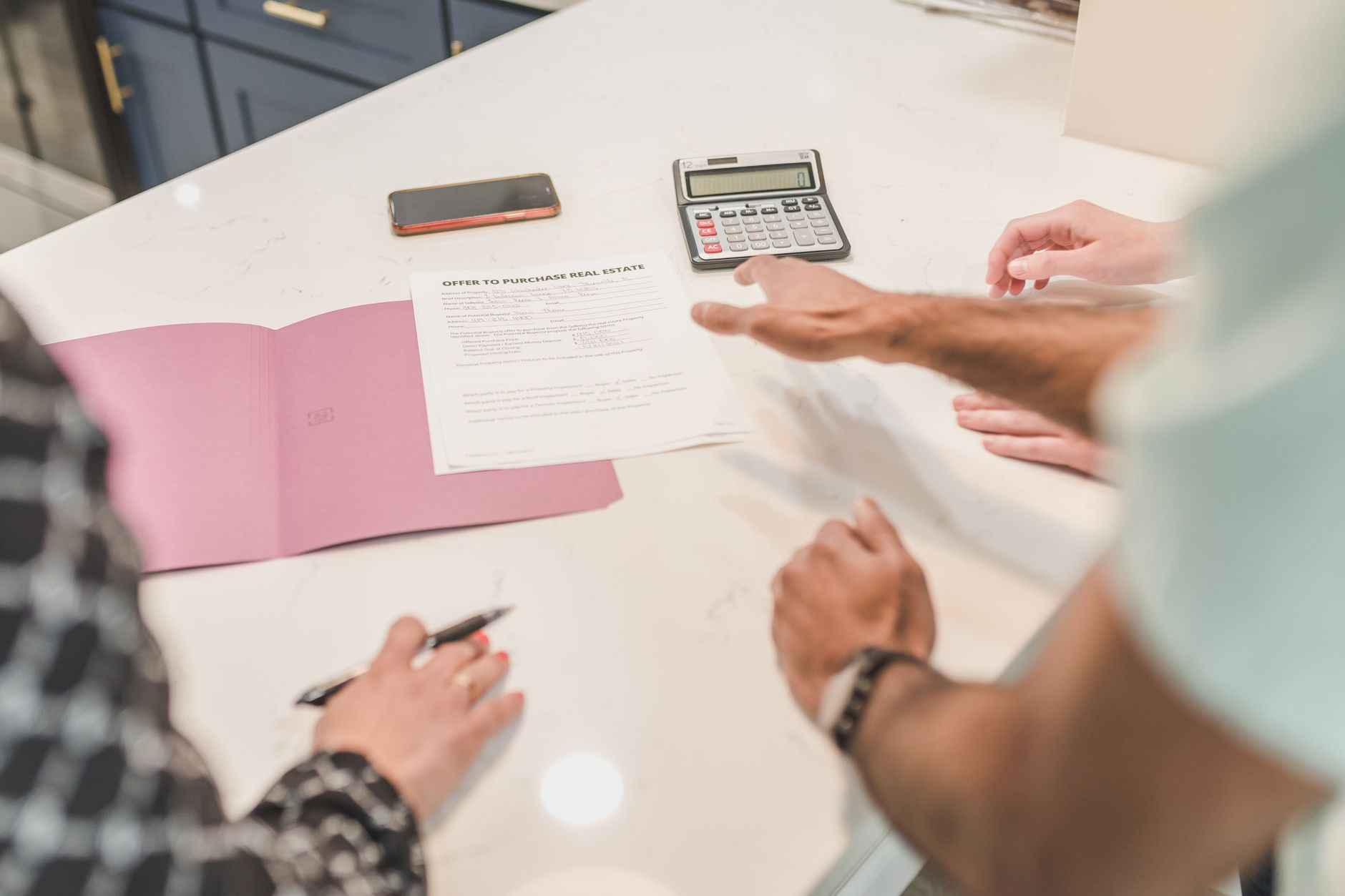

For anyone buying alone, Brussels rewards preparation more than speed. A single income gives less margin for interest-rate changes, unexpected copropriété works or a change of job. But it also simplifies some decisions: one borrower, one risk profile, one commute, one housing need. The best first step is to ask a bank or credit broker for a borrowing range, then deduct transaction costs before searching. A €270,000 apartment, close to the 2025 Brussels median reported by Statbel, can have a very different real cost depending on whether the buyer qualifies for the Brussels abatement, whether the building needs roof or lift works, and whether the monthly charges include heating. Solo buyers should request three documents early: the last general meeting minutes of the co-owners, the building’s reserve-fund position, and the energy performance certificate. In Brussels, affordability is not only the purchase price; it is the price plus the building’s future decisions.

The subject is the growing role of single-person buyers in the Brussels housing market, especially in apartment purchases. In this context, “célibataires” should be read as buyers purchasing alone or recorded without a co-buyer, not necessarily as a lifestyle label. The main institutions for readers are the notary handling the acte authentique, Brussels Fiscality for droits d’enregistrement, the SPF Finances cadastral and registration data behind official price statistics, Statbel for property and household figures, and the commune or gemeente where the buyer will register their domicile. For expats, the practical issue is not only whether a bank will lend, but whether the purchase works after costs: mortgage repayment, fire insurance, building charges, syndic fees, communal tax exposure, renovation costs, energy performance obligations and the Brussels registration-duty abatement rules.

Background

Brussels has long had a more urban housing structure than much of Belgium: more apartments, more renters, more international residents and smaller household units. Statbel’s 2026 household figures show that 46.8% of private households in the Brussels-Capital Region are one-person households, far above the Belgian average of 36.5%. That demographic reality helps explain why celibataires achat appartements is not a niche story. It reflects how the capital functions: high mobility, later household formation for some residents, separations, international work contracts, and a housing stock where apartment ownership is more accessible than family houses. The broader shift is that home ownership is no longer only a couple-based milestone. In dense European cities, one-person households increasingly shape demand, from studio and one-bedroom layouts near metro lines to two-bedroom flats suitable for remote work.

Impact

Regional — The impact is directly Brussels-based. The pattern points to a capital where apartments are the main ownership route for many one-income households, while houses increasingly sit beyond the first-time-buyer budget in many communes.

Opposing perspectives

- Single buyers and first-time owners

Many solo buyers see apartments as the only workable path into ownership in Brussels. Their argument is practical: a flat near a metro stop in Schaerbeek, Etterbeek, Anderlecht or Ixelles can reduce commuting costs, keep maintenance predictable and allow them to build equity instead of paying rent. They are usually less focused on square metres than on monthly stability, energy performance and whether the building’s charges are transparent.

- Housing affordability advocates

Tenant unions and affordability campaigners would caution that more solo purchases do not mean the market is healthy. They argue that the rise of one-income buyers can also reflect pressure: people buy smaller units because houses are out of reach, while others remain locked out entirely by deposits, bank lending criteria and competition from investors. For them, the key policy issue is not buyer behaviour but supply, public housing and price control.

- Estate agents and sellers

Agents and sellers tend to read the trend as evidence of steady demand for well-located apartments. A one-bedroom or compact two-bedroom near public transport can attract first-time buyers, separated residents, EU-quarter workers and investors. Their emphasis is liquidity: apartments in buildings with clear accounts, decent PEB scores and realistic asking prices can move faster than houses requiring major renovation.

- Banks and credit-risk managers

Lenders look less at marital status than repayment capacity. A single borrower may be perfectly bankable with stable income and savings, but the risk buffer is narrower because there is no second salary if income drops. Banks therefore scrutinise the quotité, debt-to-income ratio, employment stability, own contribution and whether the buyer has left room for charges, insurance and renovation.